Foreclosure Auction Guidelines

Once a foreclosed property has been legally relinquished from its former owner, a foreclosure is entered into an auction called a Trustee Sale (also known as a Sheriff’s Sale). While the proceedings of these auctions may seem straightforward to the casual observer, there are a myriad of intricacies, complex terminology, and strategies employed by those experienced with foreclosure auctions. This knowledge separates experienced and novice auctioneers, creating an environment with a steep learning curve. The following provides a detailed walk-through of a foreclosure auction and a few tips for succeeding at the courthouse steps.

Once a foreclosed property has been legally relinquished from its former owner, a foreclosure is entered into an auction called a Trustee Sale (also known as a Sheriff’s Sale). While the proceedings of these auctions may seem straightforward to the casual observer, there are a myriad of intricacies, complex terminology, and strategies employed by those experienced with foreclosure auctions. This knowledge separates experienced and novice auctioneers, creating an environment with a steep learning curve. The following provides a detailed walk-through of a foreclosure auction and a few tips for succeeding at the courthouse steps.

A Foreclosure Auction:

Foreclosure auctions are open to the public and are generally held at the county courthouse where the foreclosed property is located. The time and location of auctions are designated in the Notice of Sale, which is kept on record at the County Recorder’s Office and is advertised in local newspapers. At the courthouse, properties are auctioned to the highest bidder, who must pay the full sale amount in cash within twenty-four hours. There is also typically a large check deposit required at the time of sale, the amount of which is determined by the state.

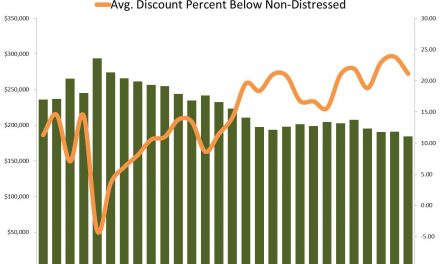

The foreclosing lender sets the opening bid at auction: an amount determined by the outstanding balance of the loan plus interest accrued and additional fees associated with the Trustee Sale (such as attorney fees). Should there be no bids equal to or higher than the opening bid, foreclosed properties are purchased by the lender. In this event, the property is labeled as Real Estate Owned. This type of sale is a common occurrence, as many foreclosed properties are not worth the amount owed to the lender due to property disrepair or depreciation.

In the event of a foreclosure auction resulting in a sale, all junior liens (property taxes excluded) are erased, i.e. 2nd mortgages. The date of recording typically determines the priority liens. If a foreclosure is purchased Real Estate Owned, the property comes with a free title.

Auction Tips:

Learn the ropes: If you’re new to the foreclosure auction world, it’s a good idea to go to the courthouse and watch the proceedings before jumping into the fray. Ask questions. Try to get a feel for what people are bidding or passing on. Counties with large urban areas have extremely competitive foreclosure auctions with many skilled professionals often representing large real estate investment groups. As many as five hundred or more properties can come up for auction in a day. Wait a few weeks before placing any bids, and learn the tips and tricks that will save you in the future.

Know what you’re bidding on: This tip pairs with the above. If a $500,000 property comes up for bid and everyone passes at $65,000, you need to know why. Maybe it’s the steal of a lifetime, but chances are there’s baggage associated with the property, such as a second lien. In instances like these, a buyer could end up purchasing several hundred-thousand dollars’ worth of debt due to the first lien. Suffice it to say that you should never bid blind.

When in Rome: Know the local state foreclosure laws backwards and forwards. Laws can differ between states regarding judicial foreclosure, deficiency judgments, and rights of redemption, just to name a few. Any and all of state law variances can affect your decision of whether or not to bid on a property. Don’t take anything for granted: Know the rules as they apply to each property and bid with no regrets at every foreclosure auction you attend.