Short sale vs. Foreclosure: 5 Things to Consider When Judging How Best to Sell your Property

So you’ve had some financial difficulty, possibly lost your job, maybe medical issues have prevented you from being able to afford the monthly payments of your loan which have resulted in the lender sending you letters threatening to foreclose. What do you do? Should you put your property up for sale? Or, what if medical issues force you to sell and you owe more on your property than what the market will bring? Should you consider Foreclosure? Short Sale? The problem is, in the battle between those two most commonly used methods for distressed sellers — Short Sale vs. Foreclosure—you’re not sure which one emerges as the winner for your situation. In order to make a wise decision, you ought to know first the following things you have to consider when trying to weigh the two options.

So you’ve had some financial difficulty, possibly lost your job, maybe medical issues have prevented you from being able to afford the monthly payments of your loan which have resulted in the lender sending you letters threatening to foreclose. What do you do? Should you put your property up for sale? Or, what if medical issues force you to sell and you owe more on your property than what the market will bring? Should you consider Foreclosure? Short Sale? The problem is, in the battle between those two most commonly used methods for distressed sellers — Short Sale vs. Foreclosure—you’re not sure which one emerges as the winner for your situation. In order to make a wise decision, you ought to know first the following things you have to consider when trying to weigh the two options.

Short sale vs. Foreclosure Round 1: Eligibility

Before anything else, you must first know if you are qualified for either of the two methods. In a foreclosure, the lender takes possession of the property after the homeowner fails to bring his mortgage payments and penalties current. On the other hand, short sales are for homeowners who may or may not be behind on their mortgage payments but no longer have enough funds to pay off the entire debt, which is more than the home’s current market value.

Short sale vs. Foreclosure Round 2: Credit Rating

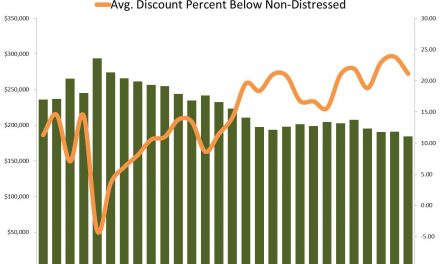

After a short sale, your potential credit rating drop is at around 50 to 150 points, with the higher drops usually due to the borrower’s backlog in the loan payment. In a foreclosure, however, credit ratings are expected to drop anywhere between 200 to 400 points. This sudden drop will usually reflect on your credit report for at least 7 years.

Short sale vs. Foreclosure Round 3: Deficiency Judgment

In a foreclosure, banks don’t usually agree to negotiate deficiency judgments after the transaction; whereas after a short sale is done, the deficiency judgment is negotiated between the bank and the seller. In some states, such as California, there is no need for deficiency judgments if the property sold through a short sale was the seller’s personal residence, which was financed primarily through purchase money.

Short sale vs. Foreclosure Round 4: Moving Out

After a foreclosure, the bank usually requires you to vacate the property immediately unless you make any prior arrangements with them. After a short sale, you are usually given 2 to 5 months before the bank requests for you to leave the property. This is because the bank takes a while to consider a short sale’s approval, thus the postponement of your moving out.

Short sale vs. Foreclosure Round 5: Future Homeownership

As long as the lender no longer requires the deficiency to be settled and the payments have been made no more than 30 days late, a seller may immediately purchase a new home right after a short sale. The only problem is it might be difficult to look for a new lender who would be willing to give a loan to you for a new house. After a foreclosure, the seller may buy a new home after 7 years without any restrictions. If he wishes to buy earlier he may do so in 5 years, but certain restrictions will be made. It is also required for a seller to report the foreclosure in all loan applications; this rule doesn’t apply with short sales.

The question is, after knowing all these, Short sale vs. Foreclosure, who wins? The answer depends on your specific financial situation. Bottom line is, it is still best to seek the advice of a professional when looking into these two considerations to know which method is best for you.